ECGI 2026: Iran War Drives Surge in Economic Crime and Geopolitical Risk Across the Indo-Pacific

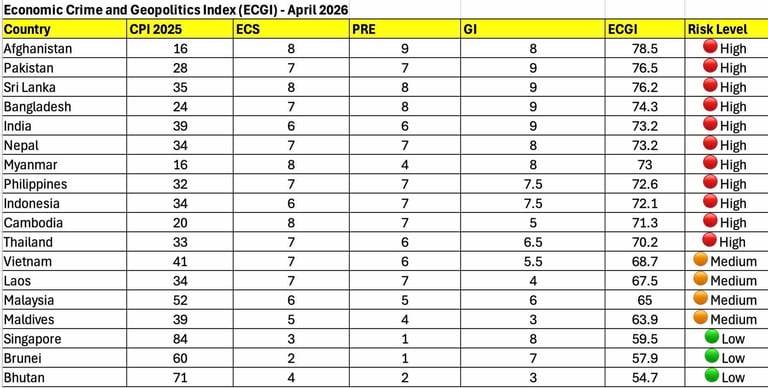

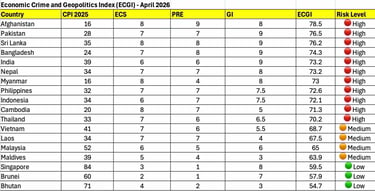

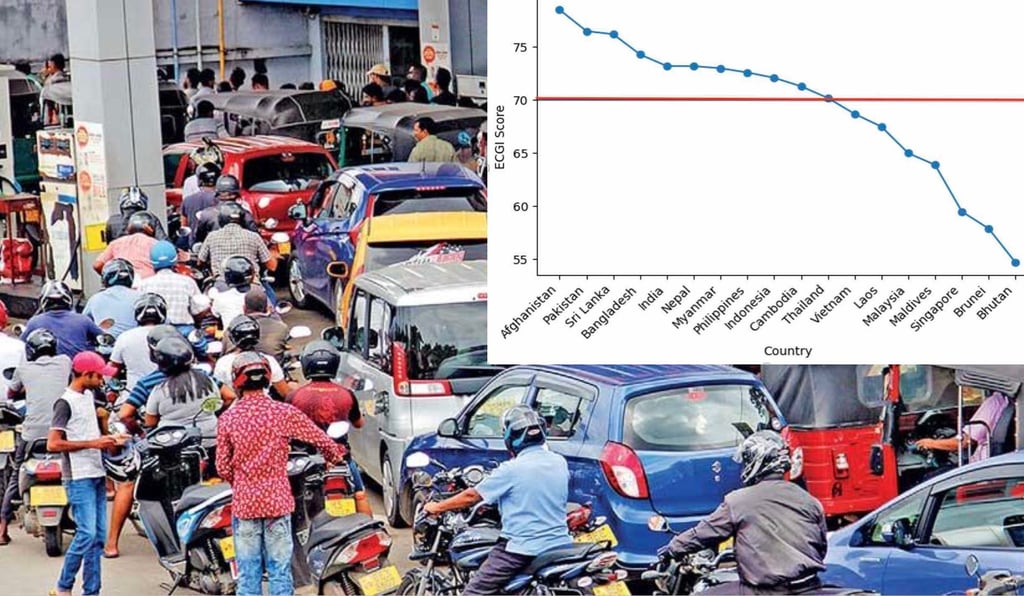

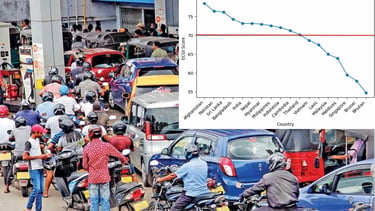

Thailand has crossed into the high-risk threshold, while the Philippines and Indonesia have further consolidated their positions within this category. South Asia continues to remain the epicenter of risk, with deeply embedded structural vulnerabilities.

NEWS

SAFN

4/5/2026

Washington, D.C. — April 5th, 2026 The latest release of the Economic Crime and Geopolitics Index (ECGI) 2026 reveals a significant escalation in regional risk across South and Southeast Asia, driven by the geopolitical shock of the ongoing conflict involving Iran. A comparative assessment between November 2025 and April 2026 indicates a clear and troubling trend: an expanding cluster of countries has moved into the high-risk category (ECGI ≥70), reflecting the growing entanglement between economic crime and geopolitical disruption. Notably, Thailand has crossed into the high-risk threshold, while the Philippines and Indonesia have further consolidated their positions within this category. South Asia continues to remain the epicenter of risk, with deeply embedded structural vulnerabilities.

This shift is not primarily the result of domestic governance deterioration. Rather, it reflects the systemic impact of external geopolitical pressures, including energy supply disruptions, rising import costs, and supply chain instability triggered by the Iran war. The disruption of key maritime chokepoints has amplified the strategic importance of Indo-Pacific economies, effectively transforming what was once a fragmented risk landscape into a continuous high-risk corridor spanning South and Southeast Asia.

A central finding of the 2026 analysis is the transformation of Geopolitical Influence (GI) from a relatively stable variable into a shock-sensitive driver of risk. This shift is shaped by three reinforcing dynamics. First, chokepoint amplification has elevated the geopolitical significance of maritime states such as Sri Lanka, Singapore, Indonesia, and Malaysia, as global energy flows are rerouted in response to conflict-related disruptions. Second, conflict spillovers have increased exposure to instability in countries such as Myanmar and Afghanistan, where regional security dynamics continue to deteriorate. Third, supply chain centrality has heightened the vulnerability of economies like Vietnam, Bangladesh, and the Philippines, whose integration into global manufacturing networks now exposes them more directly to external shocks. Together, these dynamics have driven upward adjustments in GI scores across the region, reinforcing the overall rise in ECGI values.

This regional escalation is further illustrated by comparative ECGI trends between November 2025 and April 2026. Countries such as Pakistan and Bangladesh have recorded some of the sharpest increases, rising from 74.0 to 76.5 and from 72.0 to 74.3 respectively, reflecting heightened exposure to geopolitical and economic pressures. In Southeast Asia, the Philippines has increased from 71.0 to 72.6, while Thailand has moved from 69.0 to 70.2, crossing into the high-risk threshold. The consistency of this upward trajectory across both sub-regions underscores a critical shift: economic crime risk is no longer isolated within national boundaries but is being amplified systematically across the region by external shocks. Taken together, these trends visually and analytically reinforce the emergence of a continuous high-risk corridor across the Indo-Pacific.

Sri Lanka provides a compelling illustration of the widening gap between perceived reform and actual risk exposure. While the country’s Corruption Perceptions Index (CPI) improved to 35 in 2025, its ECGI score rose from 72.88 in November 2025 to 76.2 in April 2026, firmly placing it within the high-risk category. This divergence underscores a deeper structural challenge: formal anti-corruption reforms are being undermined by persistent vulnerabilities in key sectors. The ongoing coal procurement controversy highlights this reality, with allegations of tender manipulation, substandard imports, and significant financial losses pointing to systemic weaknesses in oversight and accountability. Asanga Abeyagoonasekera, Executive Director of SAFN at the Millennium Project in Washington, D.C., observes, “Energy sector corruption during an energy crisis creates a perfect storm.” In this context, geopolitical shocks are not merely exposing governance deficits—they are actively amplifying them.

At its core, the ECGI is a composite framework built on four interrelated variables: the Corruption Perceptions Index (CPI), Economic Crime Severity (ECS), Public Response Exposure (PRE), and Geopolitical Influence (GI). By integrating these dimensions, the index offers a holistic measure of national risk that bridges the gap between internal governance indicators and external geopolitical pressures. Unlike traditional indices, which tend to assess corruption or political risk in isolation, the ECGI captures the dynamic interaction between institutional fragility and strategic vulnerability.

The broader implication of the 2026 findings is clear. Geopolitical disruption is now outpacing governance reform. While improvements in CPI scores may signal incremental progress, they are increasingly insufficient to offset the compounded pressures of energy insecurity, external conflict, and systemic institutional weaknesses. South Asia remains the most exposed sub-region, while Southeast Asia is being drawn into the same expanding risk orbit.

This is no longer a question of isolated national weaknesses, but of systemic regional convergence. The expansion of high-risk states since November 2025 signals that the Indo-Pacific is entering a phase in which economic crime, governance stress, and geopolitical disruption are mutually reinforcing. Without urgent corrective action—particularly in energy governance, procurement transparency, institutional accountability, and regional coordination mechanisms—these risks will continue to intensify. The Iran war has demonstrated that in an interconnected global system, external shocks do not remain external. They travel through energy markets, financial systems, and political structures, transforming localized vulnerabilities into regional crises. The warning is clear: geopolitical risk is no longer a background condition; it has become a primary driver of economic crime.

For more information, please visit www.southasiaforesight.net.